Market statistics for Northern Colorado, which includes Larimer and Weld counties

Ron Kuehl

Managing broker and partner, Realtec Loveland

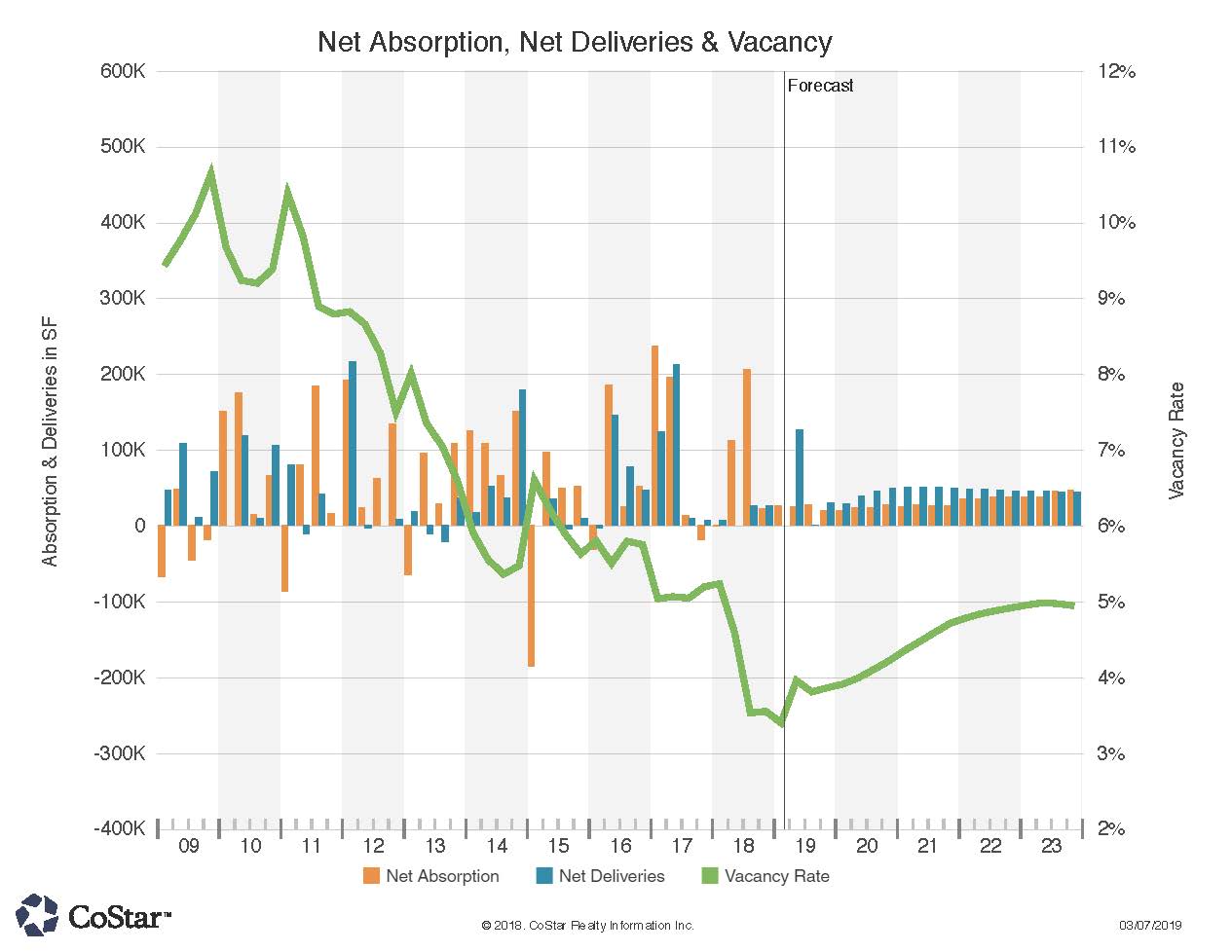

The Northern Colorado office market has grown to greater than 17 million square feet of space and 2018 ended with an overall vacancy of 3.6 percent. The Northern Colorado statistics cover Larimer and Weld counties being considered as one market. With two back-to-back years of the strongest absorption in the last decade, totaling 427,973 sf in 2017 and 339,179 sf in 2018, and very few new deliveries, occupancy rates are at historical highs. The greatest availability of office space is in the Class A office market, where new construction in 2017 and relocations into new build-to-suit deliveries drove the vacancy rate up to 8 percent. The largest share of absorption was in the Class B and C office space, which resulted in a year-end vacancy rate of 3 percent in these categories. With no speculative new construction, further economic expansion is poised to benefit Class A properties. It is anticipated that rents in Class A properties will remain relatively flat in 2019 where current triple-net rental rates are in the $18.50 to $19.95 per sf range.

Larimer County, led by Fort Collins and Loveland, ranked as the ninth-highest area in the nation for job growth in 2018, at 4.4 percent. Weld County also recorded strong job growth with a 2.6 percent increase. Nonfarm jobs in Northern Colorado grew from 274,000 to 284,100. There is a challenge of underemployment with 45 percent of the residents having a college degree and only 25 percent of the jobs requiring one. This creates opportunities for businesses considering a relocation to Northern Colorado as there are job holders in the market with the excess skill capacity ready to move up into new positions.

Despite in-migration and population growth of over 14,000 new residents in 2018, the year ended with a historically low unemployment rate of 2.3 percent. Larimer and Weld counties grew by more than 5,000 and 9,000 residents, respectively. The influx of new people is equivalent to the size of a small city, which has put upward pressure on housing prices. All four commercial sectors – retail, multifamily, industrial and office – will benefit from this job and population growth.

Since coming out of the Great Recession, developer restraint on adding new office product has led to a very healthy balance of supply with only a couple new speculative buildings coming on line in the last three years, and approximately 80 percent of this speculative space is leased. The achievable rents for new Class A office construction do not support new speculative building based upon the current high construction costs, and no new speculative office buildings have been announced to start construction in 2019. These dynamics will result in few options for expanding tenants and clearly favors landlords and sellers.

There has been a recent redevelopment trend of older office properties in Fort Collins, Loveland and Greeley that allows tenants to grow into quality Class B buildings at gross rents that are 20 percent lower than existing Class A buildings. Upgrading and redevelopment of existing structures will continue to replace new construction in 2019. With supply and demand in equilibrium, only a 3 percent vacancy and no new deliveries, Class A space will continue to be absorbed and rental rates will slowly increase in 2019.

The Centerra submarket continues to command the highest rents in Northern Colorado, and it has some of the best spaces and locations in the market for businesses seeking 5,000 to 15,000 sf. In the first two months of 2019, demand picked up with new tenants entering the market and existing businesses expanding.

With the office market in favor of landlords, tenants need to begin their search earlier and must be willing to commit quickly when they find the right space to satisfy their requirements. Tenants have been increasing their employee population density with requirements of 175 to 200 sf per employee, which puts pressure on building systems and parking. Tenants will require a minimum parking ratio of four spaces per 1,000 sf and seek locations that can provide up to six spaces per 1,000 sf. Developers should not be building or redeveloping properties that do not have at least five spaces per 1,000 square feet.

Those tenants willing to commit to lease terms without termination options of at least five years will receive the best terms from landlords. Tenants demanding shorter-term leases will have a difficult time finding acceptable space. Although many newer buildings are LEED certified, in Northern Colorado we have not found this to be a requirement and tenants are not willing to pay higher rent for LEED certified buildings.

Another trend that has not gained traction in Northern Colorado, and could be a great opportunity, is coworking space. Traditional executive suites are successful and Northern Colorado downtowns are ripe for a seasoned coworking operator.

Population and employment growth, equilibrium in supply and demand, historically low unemployment, vacancies and construction starts all clearly point to continued prosperity for the office space industry in Northern Colorado.