Taylor Coyne

Research manager, U.S. Retail, JLL

It seems that everyone still is trying to find the next big thing for retail. Some landlords focus on assembling food halls, others look at a range of entertainment concepts from virtual reality to axe-throwing. What if the answer to retail’s recent sluggishness is a trip to the gym? According to our recent research of over 6,000 fitness tenant move-ins, we’ve identified that this trend, and this larger cultural shift to a focus on wellness and healthier lifestyles, may be what retail needs to get back into shape.

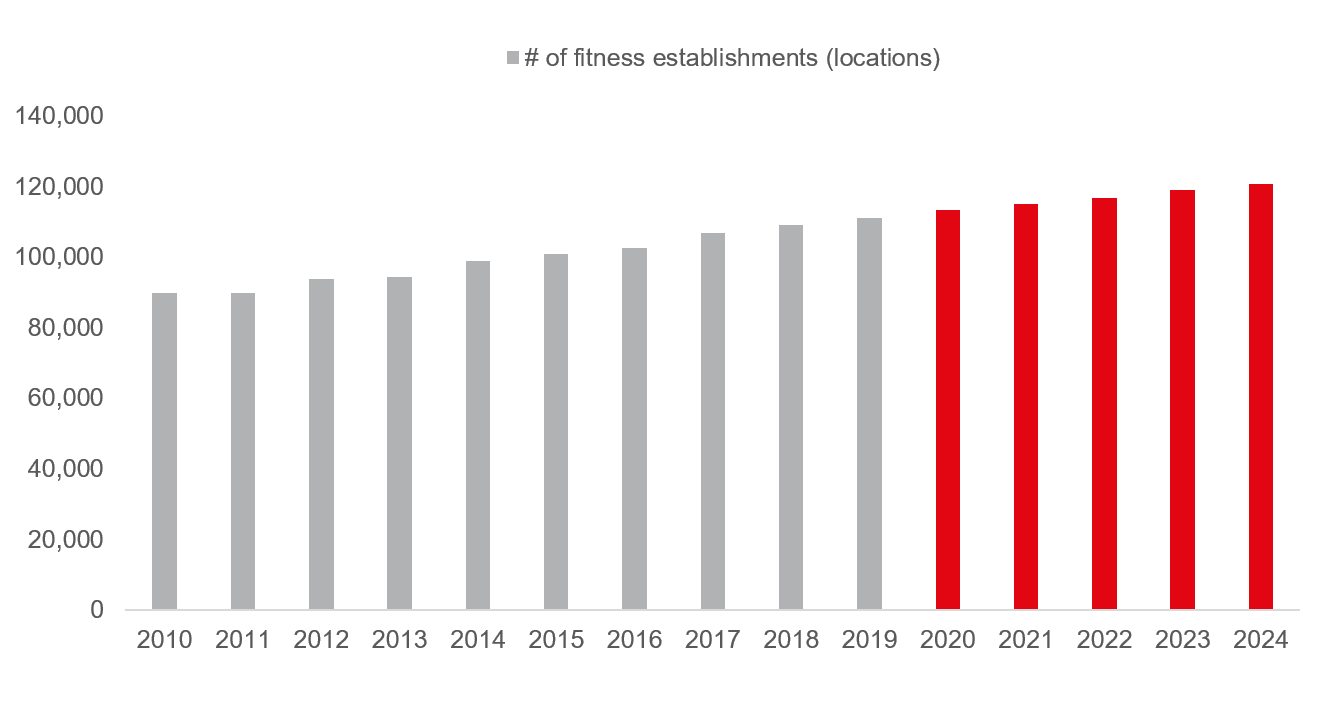

Since 2010, the number of fitness move-ins in retail locations has grown by 23.5%. This is a trend that will continue: it’s expected that the number of fitness locations will increase 8.7% to 120,700 locations by 2024, according to IBIS World.

These numbers translate into very real benefits for shopping center landlords as 47% of consumers indicated that they are motivated to visit a shopping center if it has a fitness or wellness tenant. Fitness consumers also tend to be higher earners with an average household income of $80,300. This means that savvy landlords can leverage their tenant mix to take advantage of cotenant synergies by placing wellness-focused retail tenants near their fitness center tenants.

The number of fitness locations increased 23.5% from 2010 to 2019 nationwide. Courtesy IBISWorld

As the number of fitness locations have grown over the last decade, so have the types of fitness offerings. In our research, we decided to break fitness concepts into seven different groupings: traditional, high-intensity interval training, spinning, dance, personal training, combat fitness, and Pilates and yoga. We found that specialized boutique studio concepts, often focused around a single workout activity, on average are growing six times faster than traditional gyms. HIIT, Pilates and yoga, and combat sports concepts all accounted for a higher portion of move-ins since 2013. Pilates and yoga was the category that saw the largest bump with more than double the number of openings from 2013 to 2019. This was helped by millennials who favor the social aspects of these boutique concepts.

Lower-price gym models also have been growing in popularity, accounting for hundreds of the move-ins within the last 10 years. Planet Fitness is leading the charge, opening 600 locations since 2013 with another 250 planned for the next year. Similar budget-priced options like Crunch and YouFit also have contributed to this rapid growth as landlords are attracted to the recession-proof nature of these low-cost membership models.

There also has been a shift in the types of retail properties fitness concepts are moving into. While neighborhood centers always have been a popular choice, now that subtype accounts for even more move-ins at 41.8% (compared to 34.5% six years ago). Neighborhood centers often are anchored by a supermarket, which makes it an ideal location in terms of convenience: work out and then walk next door to buy groceries and other essentials. Traditional gyms accounted for roughly one quarter (25.6%) of the move-ins to neighborhood centers in 2018, with personal training being the second-biggest category – accounting for 23.1% of all move-ins. While mall move-ins by fitness tenants accounts for a small portion of overall mall move-ins, the number of fitness locations within malls is growing rapidly – nearly tripling from 2013 to 2018.

Source: CoStar, JLL Research

All signs suggest that growth in the number of fitness locations and the focus on healthy lifestyles is not just another hot trend, as the sector has grown significantly over the past decade with signs of continued growth ahead. While the growth of at-home workout machines will have some impact on the sector, certain barriers to entry like cost and lack of space, make these options untenable to most gym goers. We believe that fitness centers will drive retail synergies, play a major role in the growing number of mixed-use retail concepts, and continue the overall trend of healthy living currently being supported by millennials and boomers alike.